Beyond the Federal Funds Rate

The Fed’s growing balance sheet tells a different story about how restrictive monetary policy really is.

At its June meeting, the Fed kept its headline policy rate unchanged at 3.5% to 3.75%.

That is the number everyone watches. It is the number markets react to. It is the number financial journalists write about.

But the same statement included another sentence that also deserves attention:

“The Committee reaffirmed its policy of maintaining ample reserves in the banking system.”

That sounds technical—and it is—but it also has important implications for the stance of monetary policy, and those implications differ from the story that makes headlines.

In short, this statement means that the Fed has directed the New York Fed’s Open Market Desk to purchase Treasury bills and, if needed, other short-term Treasury securities to maintain an ample level of reserves in the banking system.

In plain English, this means that while the Fed plans to leave the federal funds rate unchanged, it reserves the right to—and, in recent months has begun to—expand its balance sheet.

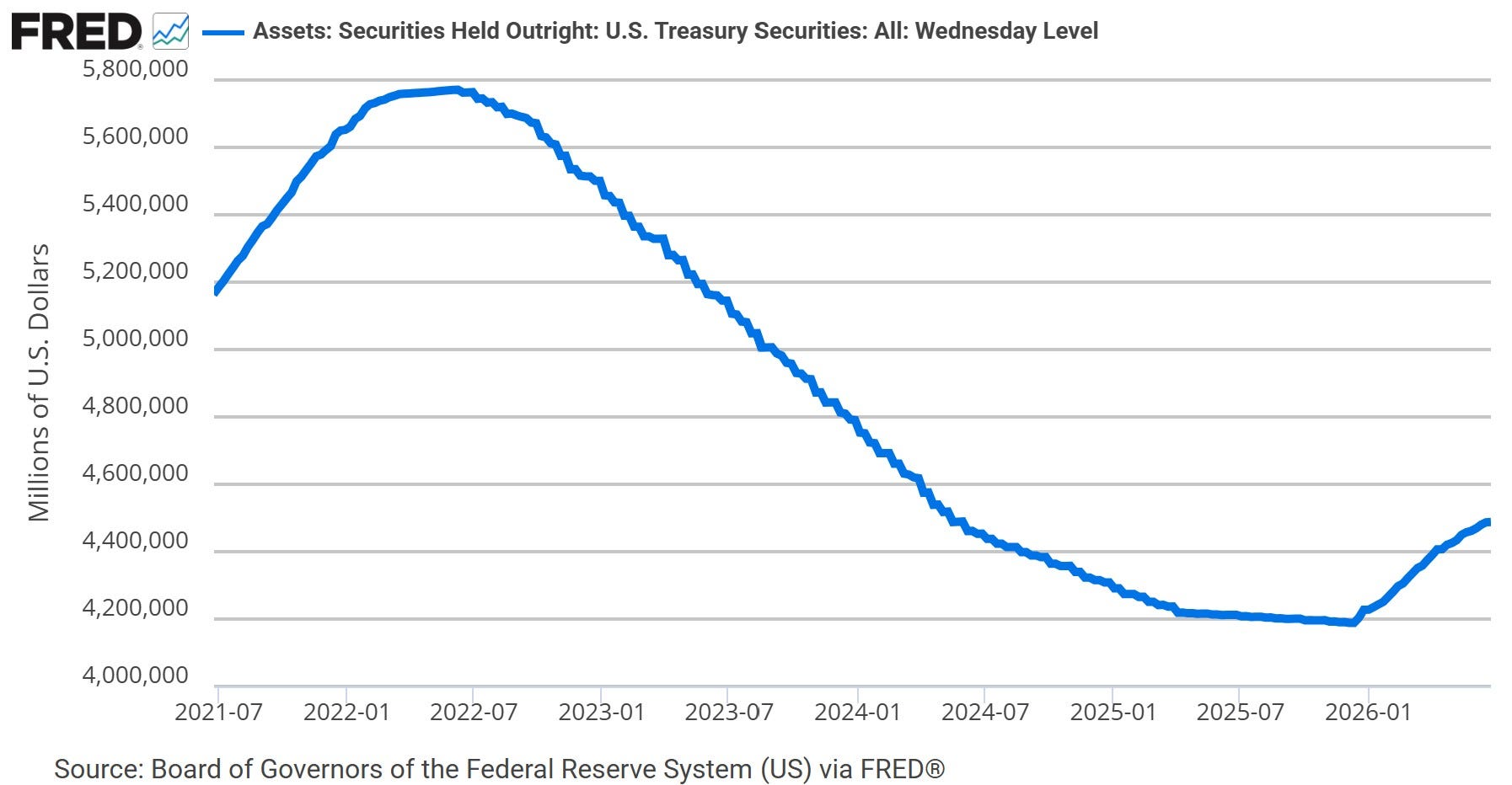

After years of balance sheet runoff following explosive growth during the pandemic, the Fed has once again become a net purchaser of U.S. Treasuries (Figure 1).

The initial pace of buying was roughly $40 billion per month. While the pace of buying has since slowed, first to $25 billion and then to $10 billion, the direction remains the same: the Fed is again adding Treasury securities to its balance sheet, thereby expanding the supply of bank reserves.

Yes, the Fed is holding the federal funds rate unchanged, but on the balance‑sheet margin monetary policy has become expansionary.

The timing of the Fed’s balance sheet expansion is also interesting.

The U.S. economy has proven quite robust following the Covid recession. The labor market remains strong and real GDP continues to grow at a moderate pace.

Inflation, on the other hand, remains stubbornly above the Fed’s 2% target. It was above target in December when the Fed resumed reserve-management purchases, and it remains above target today.

This is why the Fed’s recent move to begin expanding its balance sheet again deserves more attention. The risk is not that purchases of U.S. Treasuries will mechanically raise the price of gasoline, groceries, or rent. An increase in bank reserves is not the same thing as an increase in household income or spending. But expanding bank reserves and broader money aggregates at a time when the economy is doing well and inflation is already running above target is risky business.

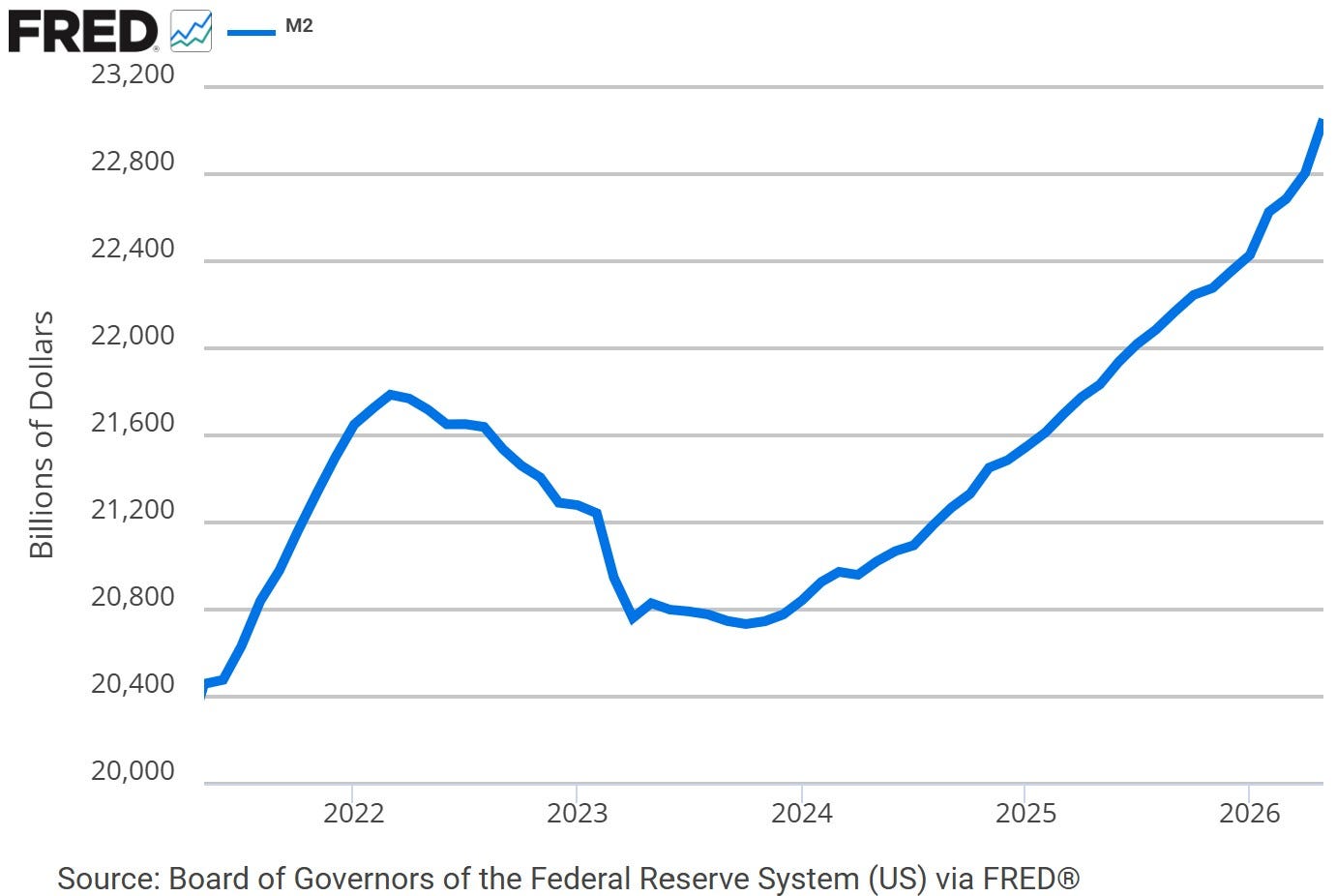

What has received less attention is evidence of accelerating money growth. Through the latest available monthly data, M2 has been growing at a noticeably faster pace than it did in 2025 (Figure 2).

When money growth accelerates during a period of elevated inflation, as we are experiencing today, it is worth asking whether policy is really as restrictive as the headline rate suggests.

This is why the Fed’s quiet balance sheet pivot matters.

Public discussion of monetary policy tends to focus on the federal funds rate because it is simple. It is the price of overnight money, and it fits neatly into a headline.

But the Fed’s balance sheet is also an important monetary policy tool. When the Fed buys Treasuries, it creates reserves. When reserves rise, the financial system becomes more liquid and the money supply tends to expand.

Under the Fed’s modern operating framework, the federal funds rate and the size of the Fed’s balance sheet don’t have to move in the same direction. The Fed can hold rates steady while increasing the supply of reserves and adding liquidity to the financial system.

The Fed’s preferred language is “reserve management purchases,” not quantitative easing. The stated goal is to maintain control over short‑term interest rates, not to push down long‑term yields or stimulate the economy. Supporters of this approach argue that elevated reserves are necessary for smooth functioning in an ample‑reserves regime, even when inflation is above target. Yet implementation and the stance of monetary policy are not fully separable: reserve management purchases influence money growth.

The Fed is buying Treasuries. Bank reserves are rising. Money growth is accelerating. The federal funds rate may be unchanged, but on the balance‑sheet margin, the Fed has moved in an expansionary direction.

If you enjoyed this mildly efficient and occasionally rational take on the Fed’s recent move to expand its balance sheet and what it implies about the stance of monetary policy, consider subscribing below. We’ll keep exploring markets and models, uncovering mildly surprising truths along the way.

No hot takes; just thoughtful ones.

About the Author: Seth Neumuller is an Associate Professor of Economics at Wellesley College where he teaches and conducts research in macroeconomics and finance. He holds a Ph.D. in economics from UCLA. His Substack is Mildly Efficient (and Occasionally Rational) where he explores topics in finance and macro from first principles, cutting through complexity with clear, grounded analysis.

Notes and Sources

AI tools were used to edit prose; all figures are straightforward to reproduce from the cited sources.