The Hedging Value of Long-Term Treasuries Varies Over Time

What 2022 taught us about the diversification value of long-term U.S. government bonds.

TL;DR: Long-term U.S. Treasuries are often treated as the natural hedge against stock market risk. But their diversification value depends on the stock-bond correlation, which changes over time. When the correlation turns positive, long-term Treasuries can lose much of their value as portfolio insurance.

We teach undergraduates that U.S. Treasuries are the closest thing we have to a risk‑free asset.

This is true in a very specific sense. If you buy a short-term U.S. Treasury bill and hold it to maturity, you can be reasonably confident about the dollar payoff you will receive. The U.S. government is unlikely to default on short-term Treasury debt.

But this basic lesson can easily lead to a misleading conclusion.

If Treasuries are “risk-free,” then it is tempting to think that they are also a reliable hedge against stock market risk. After all, if the payoff is safe, then Treasury returns should be uncorrelated with the return on risky assets like stocks.

The problem is that a three-month Treasury bill and a thirty-year Treasury bond are very different assets. The former is close to risk-free if held to maturity. The latter can fluctuate substantially in value in response to changes in interest rates.

Indeed, many investors learned the limits of this idea the hard way in 2022, when both stocks and long‑term Treasuries fell at the same time.

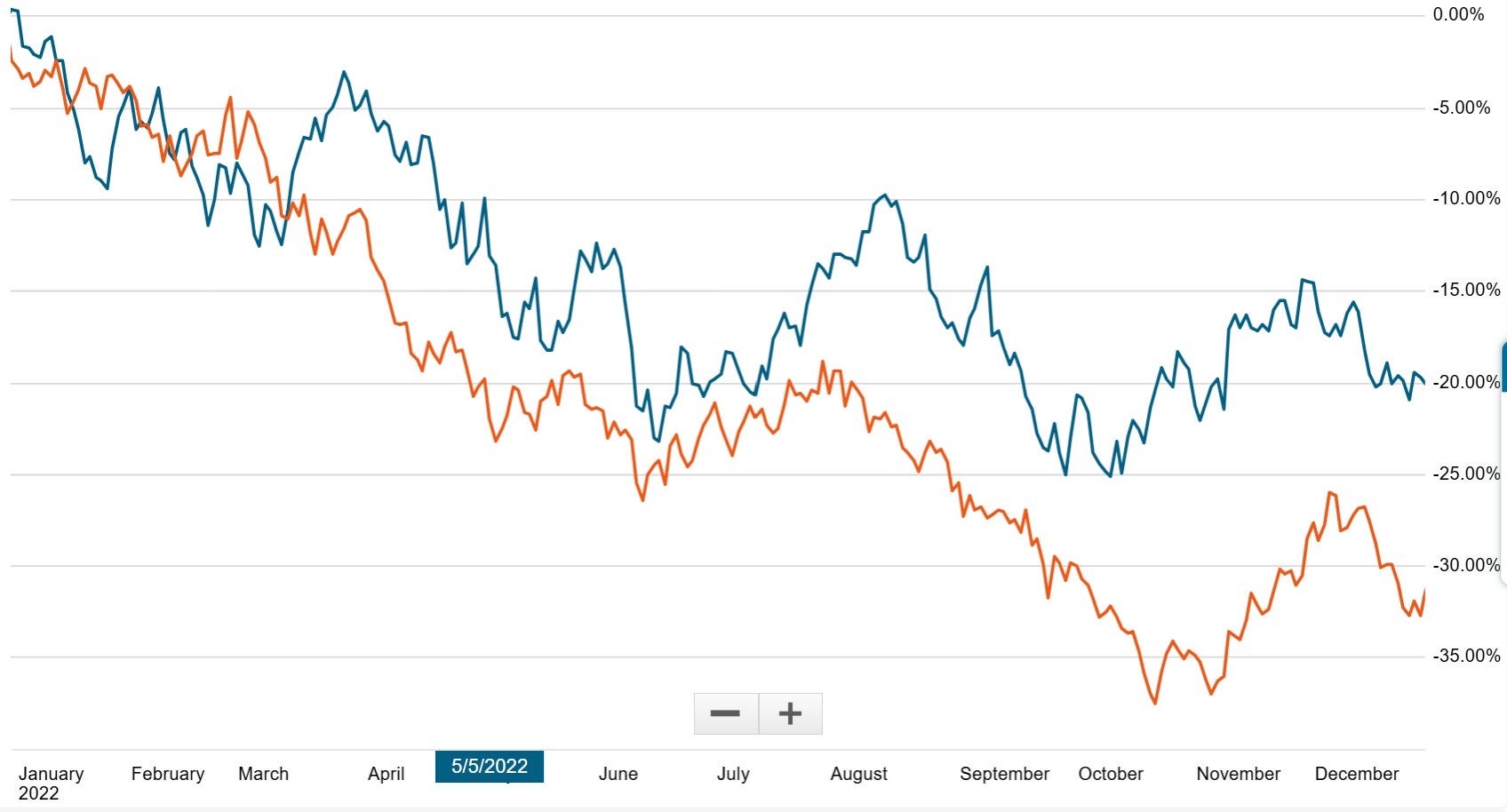

In 2022, inflation forced the Federal Reserve to hike interest rates from near zero to north of 5 percent by mid-2023. Long-term U.S. Treasuries got hit hard. TLT, a widely followed ETF that holds long-term U.S. Treasury bonds, lost roughly 31 percent of its value during calendar year 2022. Stocks also fell sharply, with the S&P 500 down about 20 percent for the year (Figure 1).

This combination made 2022 a painful year for the classic 60/40 portfolio. More importantly, it was a reminder that long-term U.S. Treasuries can fail to hedge stock market risk precisely when investors need it the most.

Was the experience of 2022 an anomaly? Or is positive comovement between stocks and long-term Treasuries a common occurrence?

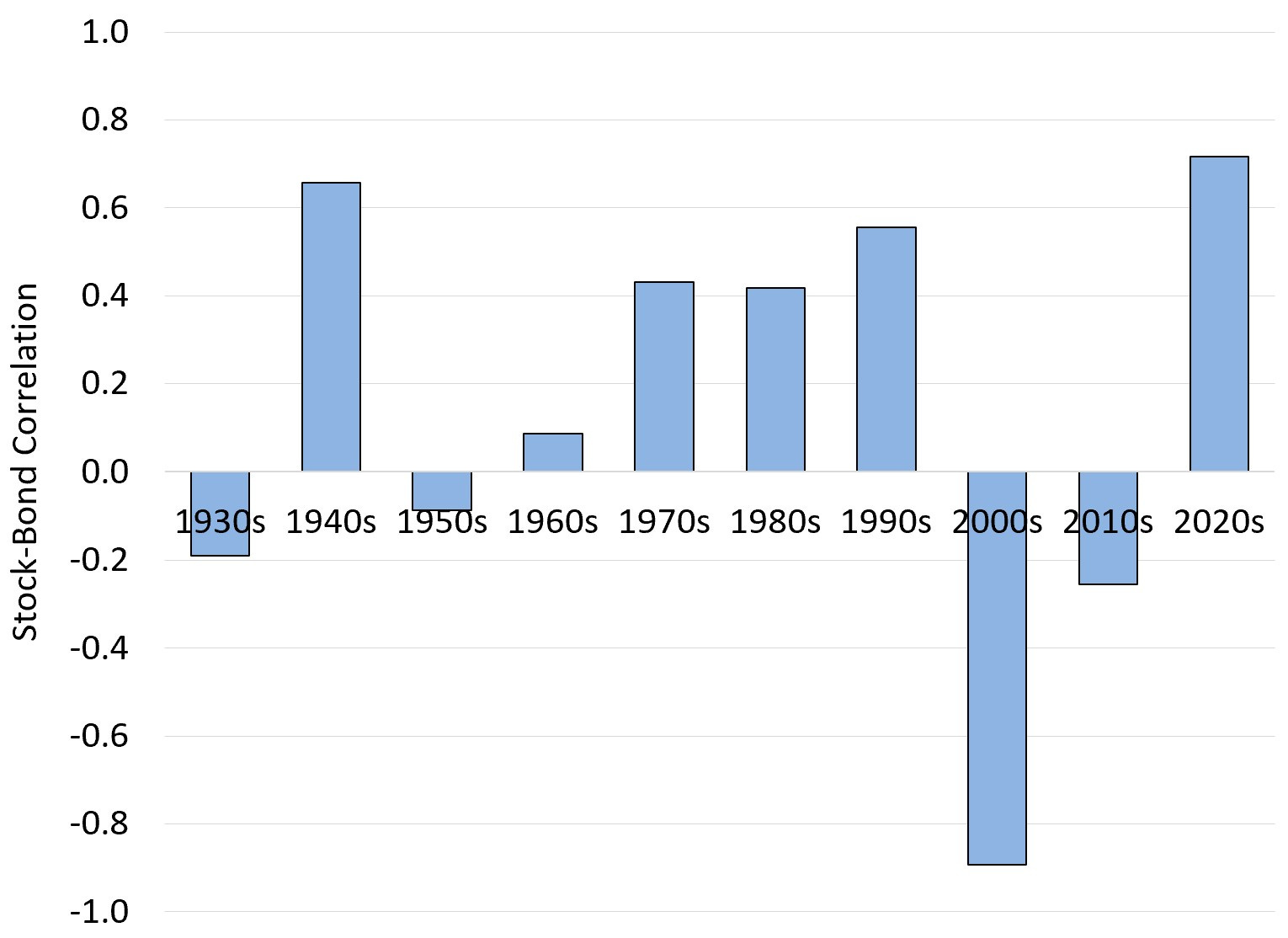

Figure 2 reports the correlation between total annual real returns on the S&P 500 and 10-year U.S. Treasury bonds by decade, from 1928 through 2025.1

When the stock-bond correlation is negative, long-term Treasuries can reduce portfolio risk in two ways: they are less volatile than stocks, and they tend to rise when stocks fall.

When the correlation turns positive, investors still get the lower volatility of bonds, but they lose the second benefit. Bonds no longer provide the same insurance against equity-market losses.

The striking feature of Figure 2 is not simply the recent switch from negative to positive comovement between stocks and bonds. It is that the strong negative correlation of the 2000s and 2010s was more of an anomaly than a regularity. Over most of the last century, the stock-bond correlation was positive, not negative.2

Yet the standard intuition about U.S. Treasuries as a portfolio hedge is based on the premise that the stock-bond correlation is negative and will remain that way into the indefinite future.

Long-term Treasuries are valuable hedges when their correlation with stocks is negative, as it was during the 2000s and 2010s. They are much less valuable as a hedge when their correlation with stocks is positive, as it appears to be now and as it was during the 1960s, 1970s, 1980s and 1990s. In other words, the hedging value of long-term Treasuries depends critically upon the current stock-bond correlation regime.

This has important implications for retirees and those nearing retirement.

If stocks and long-term Treasuries tend to fall at the same time, as they did during 2022, retirees face the very outcome diversification was meant to avoid: the real possibility of a large decline in wealth at the worst possible time.

There is also a broader lesson here about how we talk about safe assets.

U.S. Treasury bills are close to risk-free over short horizons. Long-term U.S. Treasury bonds are not. They are safe from default risk, but they are not safe from interest-rate risk. And because interest-rate risk is sometimes tied to the same macroeconomic forces that move stock prices, long-term Treasuries do not always offer reliable portfolio insurance.

A few practical implications follow from these observations.

First, the role of long-term Treasuries in a portfolio should reflect the possibility that the stock-bond correlation can change.

Second, for retirees and those nearing retirement, relying on long-term Treasuries as insurance against an equity market downturn is risky.

Third, “correlation risk” can increase the appeal of short-term Treasuries for retirees and those nearing retirement. Shorter duration Treasuries expose investors to less interest rate risk, though they also typically offer less income than long-term government bonds.

None of this eliminates the case for including long-term U.S. government bonds in a portfolio. They offer a stable income stream and can reduce overall portfolio volatility.

But history tells us that the stock-bond correlation is not always negative. It has evolved over time, will likely continue to evolve, and has been positive more often than negative over the last century.

More importantly, long-term Treasuries are not risk-free, and they are certainly not a universal hedge against stock market risk. Investors and professors, take note.

If you enjoyed this mildly efficient and occasionally rational take on time-variation in the hedging value of long-term U.S. Treasuries, consider subscribing below. We’ll keep exploring markets and models, uncovering mildly surprising truths along the way.

No hot takes; just thoughtful ones.

About the Author: Seth Neumuller is an Associate Professor of Economics at Wellesley College where he teaches and conducts research in macroeconomics and finance. He holds a Ph.D. in economics from UCLA. His Substack is Mildly Efficient (and Occasionally Rational) where he explores topics in finance and macro from first principles, cutting through complexity with clear, grounded analysis.

Notes and Sources

This piece draws on ideas from my working paper on time-varying stock-bond correlations and life-cycle portfolio choice, which studies how persistent changes in the stock-bond correlation affect optimal bond holdings over the life cycle.

AI tools were used to edit prose; all figures are straightforward to reproduce from the cited sources.

Correlation is a statistical measure of how much two data series move together, or not. It varies between -1 and +1, where a negative value means that the two data series tend to move in opposite directions, whereas a positive value means that the two data series tend to move together.

The annual correlation between total returns on the S&P 500 and 10-year U.S. Treasuries between 1928 and 2025 is slightly positive at 0.09.

I’m curious about your first point. If stock-bond correlations have been negative for much of recent history, why do you place so much emphasis on portfolios being prepared for that relationship to flip?

Are there particular economic indicators or market conditions that would make you think a shift back to a positive correlation is becoming more likely? Or is the idea simply that investors should always account for that possibility, even if the odds seem low?