Will Higher Energy Prices Lead to Persistent Inflation?

Money-supply data suggest this inflation scare is more likely to be transitory than persistent

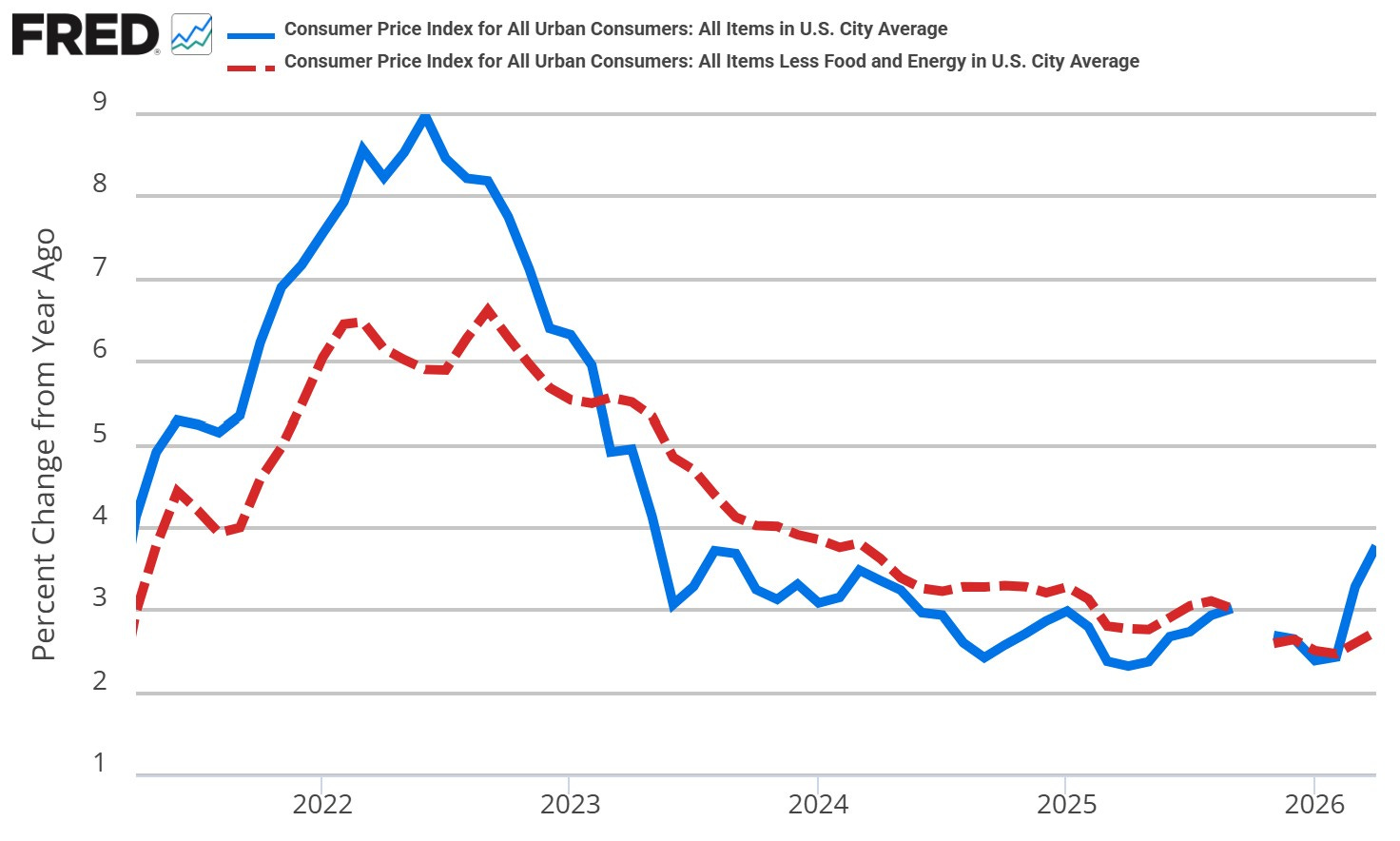

The April CPI report was ugly. According to the U.S. Bureau of Labor Statistics, consumer prices rose 0.6 percent in April, pushing year-over-year CPI inflation to 3.8 percent (Figure 1).

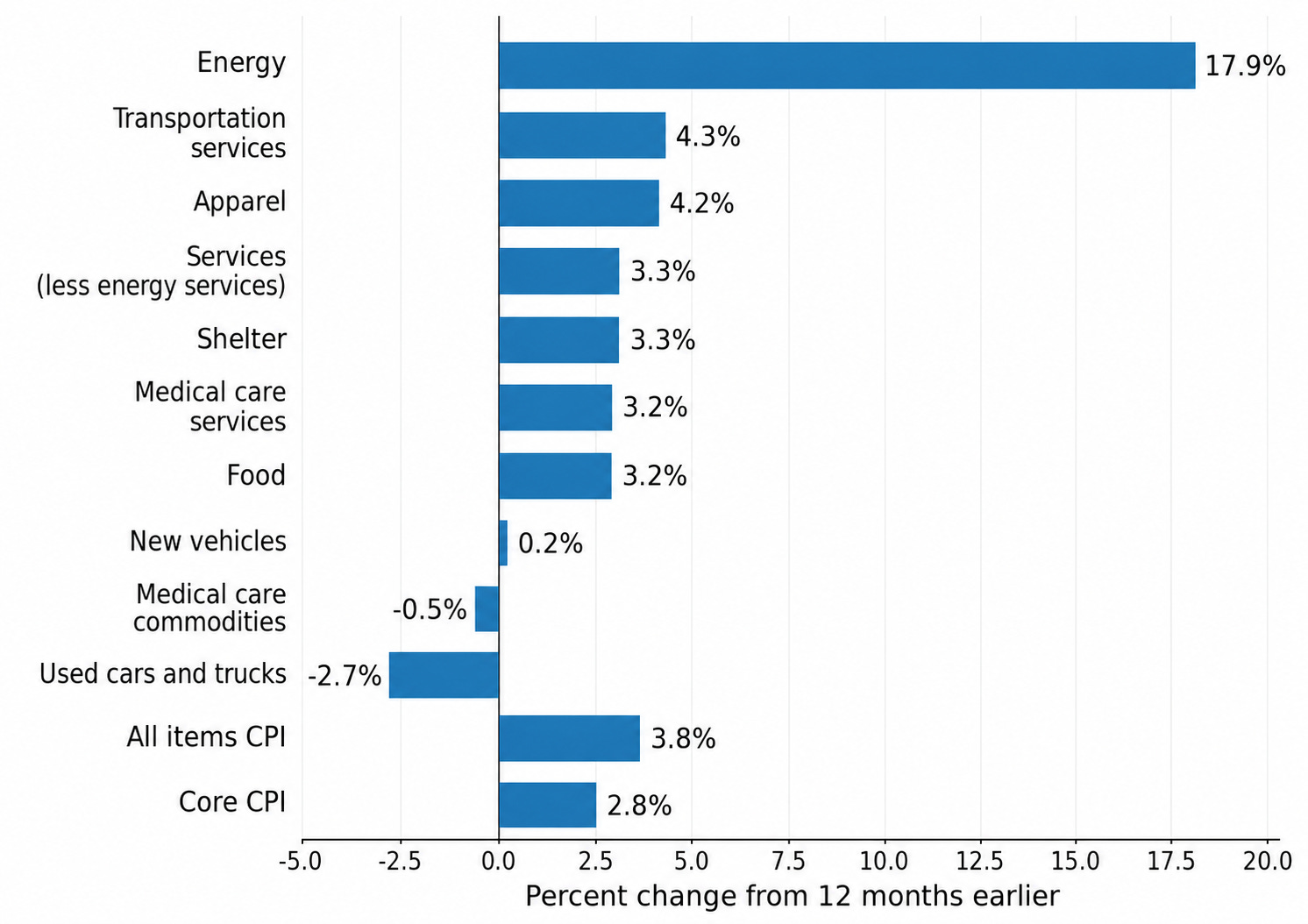

Energy prices were the main culprit (Figure 2). The energy index rose 3.8 percent in April alone, accounting for more than 40 percent of the monthly increase in the all-items index, and is up 17.9 percent over the past year. Within energy, gasoline prices rose 5.4 percent in April versus March, and are up 28.4 percent over the past year. Fuel oil, commonly used for heating in the northeast, was up 5.8 percent in April compared to March, and is up 54.3 percent over the past year.

Energy accounts for about 7 percent of the CPI basket, but because energy prices rose nearly 18 percent over the past year, they contributed roughly 1.3 percentage points to the April headline year-over-year inflation rate. Without the increase in energy prices, all-items CPI inflation would have been closer to 2.5 percent.

Energy prices matter, not just for transportation and heating costs, but because energy is an input into transportation, production, and distribution of goods and services throughout the economy. If energy prices rise sharply enough, the price of filling your tank rises first, followed by the cost of shipping groceries, flying on airplanes, heating buildings, and producing energy-intensive goods. As price increases begin to spread throughout the economy, the fear is that workers will demand higher wages to maintain purchasing power, firms will raise prices to cover higher labor costs, and the economy will slide into the much dreaded wage-price spiral.

Still raw from Covid-era inflation, it is completely understandable for consumers and media pundits to be worried that we might be in for another painful and persistent rise in prices. And yes, it is quite possible that year-over-year headline CPI inflation tops 4 percent later this year if the war with Iran is not resolved and the rise in input costs begins to cause price hikes in sectors of the economy outside of energy.

But are we in for persistent inflation that will adversely impact the U.S. economy and require the Fed to intervene by hiking interest rates?

On this question, I am far less convinced that we are looking at a repeat of our Covid-era inflation experience. At the risk of throwing salt in healing wounds, this time inflation is in fact most likely transitory.

The rise in headline inflation since the onset of the war with Iran is best understood as a classic supply shock. The closing of the Strait of Hormuz has restricted the flow of oil into global energy markets, pushing up the price of energy and energy-intensive inputs. That matters. But it matters because it changes relative prices. Energy becomes more expensive compared with everything else.

All else constant, this is what economists call a relative price shock. The spike in energy prices has made energy, and those goods and services which rely heavily on energy as inputs, more expensive relative to everything else.

A relative price shock can raise the price level. It can even produce several uncomfortable CPI prints. But by itself, it does not necessarily produce persistent inflation.

The key insight is that households and firms only have so much money to spend. And because the demand for energy is relatively inelastic—we all still need to drive to work, heat our homes, and keep the lights on—households and firms will have to cut back on their spending on everything else in order to pay more for energy. Put simply, when energy becomes more expensive, there is less room in the budget for everything else. This tends to put downward pressure on prices outside of the energy sector, thus blunting the pass through of higher energy costs into final prices.

Contrast this with what happened during the Covid recovery. The initial increase in prices was also the result of a supply shock. Supply chains had become snarled due to intermittent economy-wide closures, semiconductors became incredibly scarce, and consumers bid up the price of everything in short supply from couches to cars.

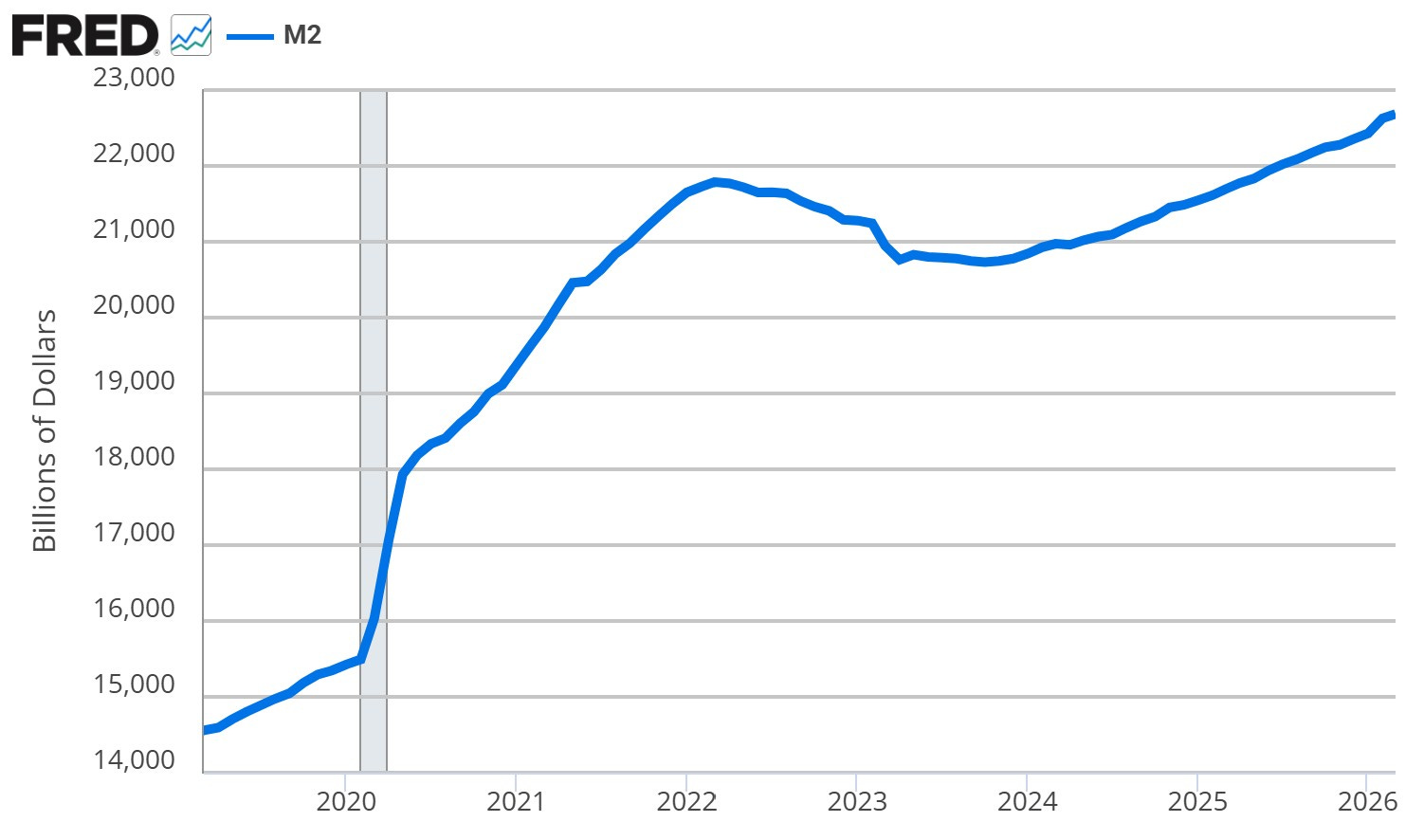

But what made these initial price increases more persistent was that the supply shock occurred alongside an enormous expansion in nominal purchasing power. Between February 2020 and March 2022, M2 rose by more than 40 percent, reflecting the combined effects of fiscal transfers, emergency monetary policy, and the broader response to the pandemic.

That is not to say this monetary expansion wasn’t justified. Indeed, much of the broader monetary expansion reflected the combined effects of fiscal support, Treasury issuance, and Federal Reserve asset purchases during the pandemic. But without highly accommodative monetary policy, the initial bout of inflation would most likely have been transitory. Prices of those goods most impacted by supply constraints would have risen sharply, but these price increases would have quickly dissipated as supply chains became unsnarled and, more importantly, inflation would not have become widespread. Instead, what happened was that headline inflation rose above 3 percent in March 2021 and it did not return to levels below 3 percent until June 2024, more than three years later, largely as a result of accommodative monetary policy.

This is not the environment we find ourselves in today.

Money growth has been broadly contained over the past two years (Figure 3). According to data from the Federal Reserve Bank of St. Louis, M2 grew at an average annual rate of just 4.0 percent between April 2024 and April 2026. That is not the kind of monetary growth one would normally associate with a self-reinforcing inflation spiral. In fact, it is consistent with the Fed’s 2 percent inflation target given a growth rate of real GDP in the neighborhood of 2 percent.1

There is one recent development which is worth watching, however.

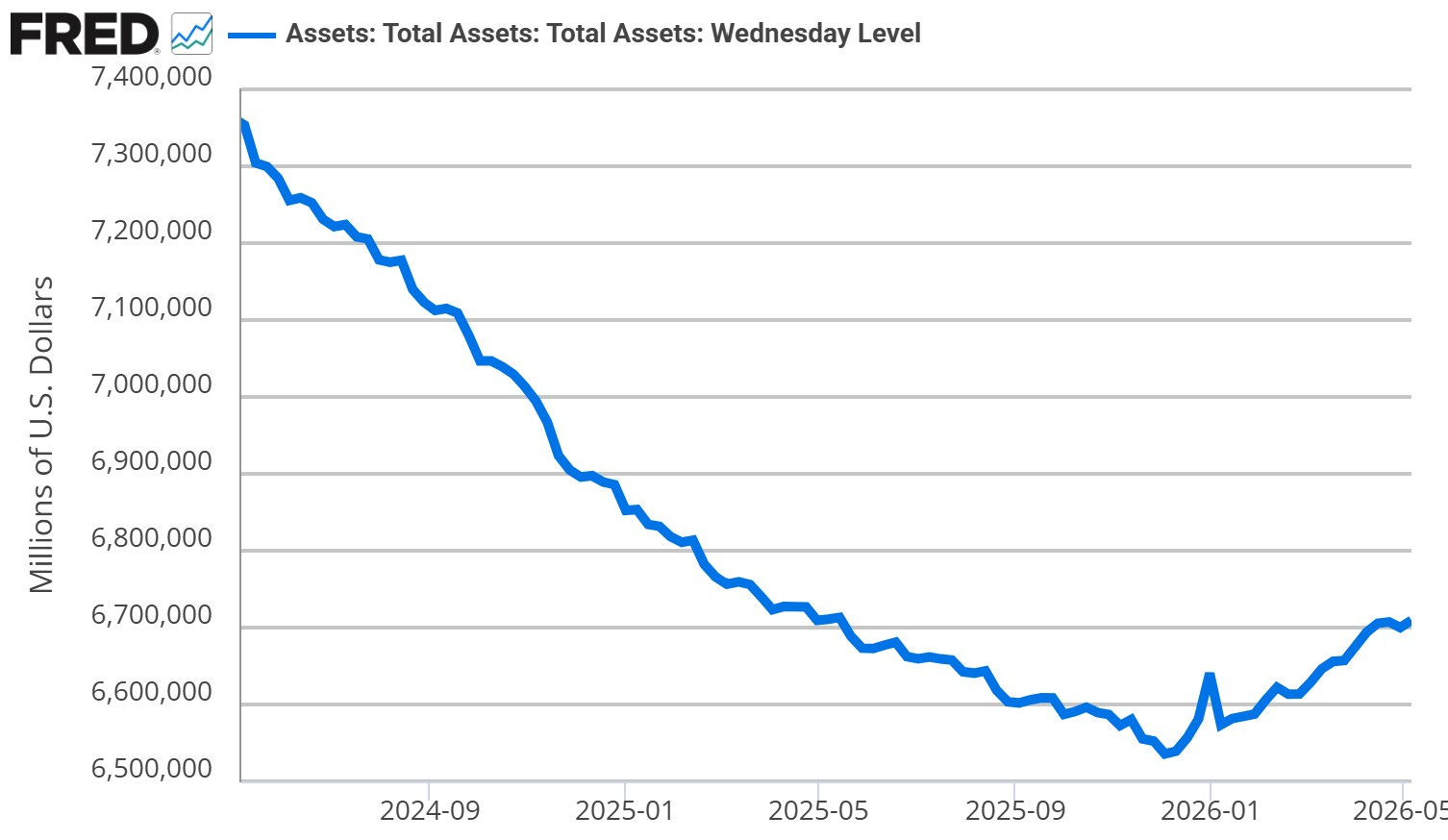

After years of quantitative tightening, the Fed’s balance sheet has recently begun expanding again (Figure 4). Even though the Fed has kept its headline policy rate steady, citing upside risks to inflation from the war with Iran combined with a remarkably resilient labor market, its balance sheet has begun to grow once more. This matters because balance sheet expansion can eventually show up as faster money growth.

The Fed’s stance is not as restrictive as the policy-rate discussion alone might suggest. Since the start of the year, the Fed’s balance sheet has expanded by roughly $175 billion. While this is not a huge amount given the Fed currently holds north of $6.7 trillion worth of securities on its balance sheet, it does represent a marked shift in policy that is worth taking note of and watching closely going forward. So far, though, the recent balance‑sheet growth has not yet translated into a visible acceleration in the growth rate of M2 (see Figure 3).

Whether this marks the beginning of a new easing cycle or a temporary technical adjustment matters. If balance-sheet expansion continues and begins to feed through into broader money growth, the argument that this inflation episode will remain transitory becomes weaker.

If the Fed’s balance-sheet expansion were to accelerate, what currently looks like transitory inflation induced by an oil supply shock could turn into a more persistent inflationary problem.

If growth in the money supply remains contained, however, then consumers and firms will be forced to reallocate spending. More money going toward energy means less money going elsewhere. In that environment, inflation can rear its ugly head without becoming a self-perpetuating problem.

That is very different from a world in which nominal purchasing power is expanding rapidly and higher prices are fueled by continued spending growth.

This is why I would be cautious about extrapolating too much from the April CPI report. The report was bad. The energy shock is real. Inflation risk has increased. But the case for a return to Covid-era inflation remains weak.

The economy is facing an energy-price shock. The April CPI report makes this crystal clear. But it does not yet look like we are in for a persistent bout of inflation.

That could change if monetary policy becomes more accommodative. For now, though, the money-supply data suggest this inflation scare will most likely turn out to be transitory, not persistent.

If you enjoyed this mildly efficient and occasionally rational take on whether the recent spike in energy prices is likely to generate a persistent rise in inflation, consider subscribing below. We’ll keep exploring markets and models, uncovering mildly surprising truths along the way.

No hot takes; just thoughtful ones.

About the Author: Seth Neumuller is an Associate Professor of Economics at Wellesley College where he teaches and conducts research in macroeconomics and finance. He holds a Ph.D. in economics from UCLA. His Substack is Mildly Efficient (and Occasionally Rational) where he explores topics in finance and macro from first principles, cutting through complexity with clear, grounded analysis.

Notes and Sources

AI tools were used to edit prose; all figures are straightforward to reproduce from the cited sources.

If real GDP growth averages 3 percent, then 4 percent growth in the money supply is consistent with an inflation rate of just 1 percent in the long run.